Several years ago, I observed a friend as he sat down at Turning Stone Casino to play Blackjack. I am not a gambler myself (I’ll get into that later) but we were there for dinner, and he decided to play a few hands before we were seated. He was an avid player and more than familiar with basic strategy, however luck was not his friend that night. I enjoy watching Blackjack because it is a dynamic game of shifting percentages. Every card dealt changes the odds of success for the player. Ed Thorp, the “Father of Blackjack strategy” as well as a highly successful money manager wrote the seminal book on Blackjack betting, Beat the Dealer back in 1962 in which he gave readers the odds for how to bet depending on what their starting hand was and what the dealer was holding. My friend followed this strategy perfectly. He held at 16 when the dealer was showing a 4, only to have the dealer uncover a King and drop a 5 on it. He held at 20 and watched the dealer draw a 21. On and on this went until eventually my friend threw in the towel and left the table.

This story comes to mind because lately the stock market has punished prudent investors and rewarded those who are betting against the odds. The stock market, like Blackjack, is a game of shifting percentages in which, what happened in the past affects your potential outcomes going forward. A well-known commentator on CNBC recently dismissed the idea of certain stocks being overvalued as “Gambler’s Fallacy”. This cannot be further from the truth! The Gambler’s Fallacy describes assigning probabilities when the outcome is statistically independent. An example in the casino would be playing roulette and betting on Red just because Black has come up 5 times in a row. This commentator thought that just because XYZ stock was up 5 days in a row, this did not change the odds of it being up the next day. Wrong! Excess gains in the market today are simply borrowing from gains tomorrow. A stock, or a market writ large, has an intrinsic value based upon its earnings and the competing risk-free interest rate. The P/E ratio can change depending on sentiment, a change in the earnings growth rate, or even price momentum BUT eventually the market price will come down to a rational value. Put simply, in the short-term market prices can behave like an intemperate child, but in the long-term the market is a rational pricing mechanism.

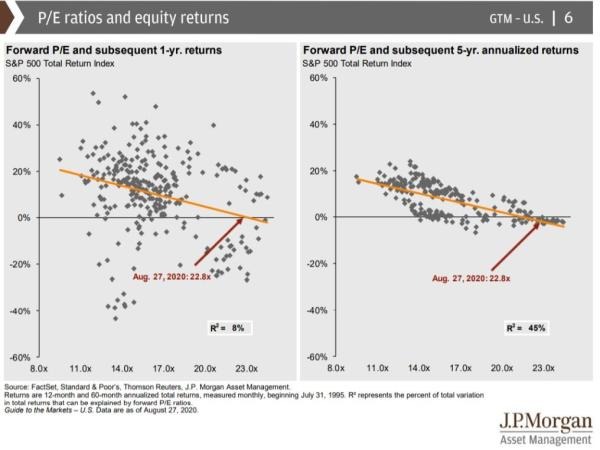

The stock market is often paralleled to the likes of a casino. This comparison is especially flaunted during periods of increased speculative interest in stocks. People find it amusing that I work “in the stock market”, yet I do not consider myself a gambler. At the casino, the longer you play the greater the odds shift toward the house winning. Stock market investing has the exact opposite characteristic, in that the less you trade, the greater your odds of success. Furthermore, if you follow the rules of value investing and buy stocks for a price at which you can rationally discount future earnings, you surely increase your odds of success. When it comes to investing, there is no crystal ball, however there is a noteworthy correlation between current valuations and realized stock returns. The above chart illustrates the relationship between Forward P/E and subsequent 1- and 5-year returns.

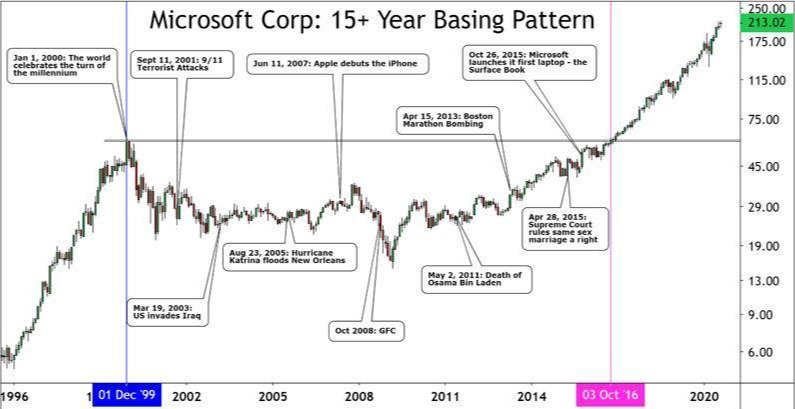

Our team is frequently asked, “How is the stock market doing so well when the economy is struggling so much?” The answer is simple, market indices are being strongly influenced by only a handful of stocks. Apple, Microsoft, Amazon, Alphabet, and Facebook now make up close to 25% of the value of the S&P 500 Index. This is an even higher percentage than the top 5 stocks in year 2000 ahead of the epic drop in the Nasdaq. We are not predicting a stock market crash any time soon, but we are suggesting that there are other areas of the market that have failed to fully participate in the summer rally, areas that offer substantially better risk-reward in the long-term. Back in 2000, investors who bought Microsoft at the top waited over 14 years to break even. Investors in Cisco at that top still have not recovered their initial investment. Can these names continue to climb higher from here? Perhaps. Sentiment and momentum can move prices well above rational metrics in the short-term, just as you can sometimes make money in Blackjack when you hit on 18. Longer term though, you may want to consider playing the odds by re-balancing some of those Tech stock gains into more reasonably valued sectors. We look forward to discussing this with you.