Welcome to the first edition of the Michael Roberts Associates Technical Corner bulletin. Each quarter for the remainder of 2021, we’ll review global market developments through the lens of technical analysis. Now, what is technical analysis? Technical analysis is the study of price action and trends within capital markets. This is performed by evaluating the economic forces of supply and demand (sellers & buyers). To learn more about the discipline, I suggest you check out the CMT association website.

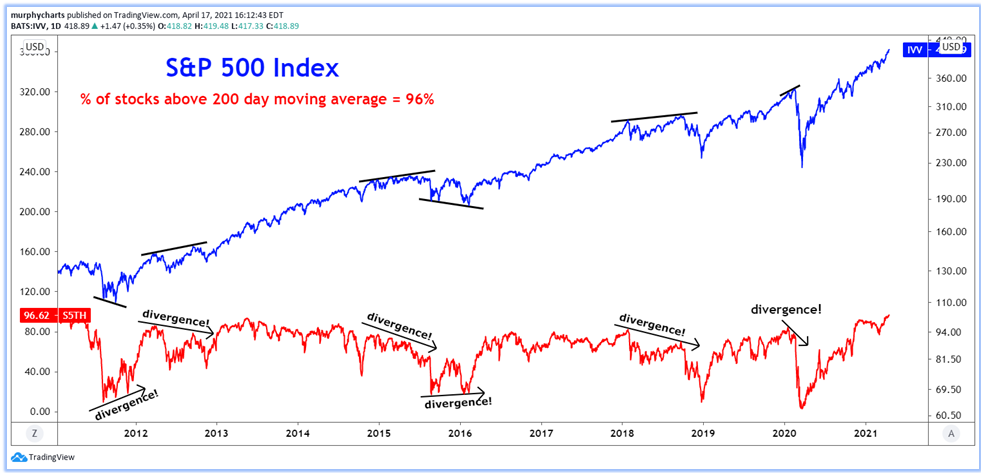

So, let’s get started! We’re a few weeks into Q2 and there remains an insatiable risk appetite for US equities. The below chart outlines the S&P 500 and the percentage of stocks above their 200-day moving average. Moving averages help us not only identify trend direction, but the strength of trend as well. If a specific stock index is printing new 52-week highs, but the percentage of stocks above their respective 50 or 200-day moving average is declining – this would constitute a bearish divergence. It is signaling that although the index is forming new highs, not all of its constituents are necessarily participating in the move higher. During the recent rally in the S&P 500, the percentage of stocks that were trading above their 200-day moving average reached its highest level in over 15 years. That is one strong move!

European Banks at Resistance

Next up, we’d like to briefly touch on the MSCI Europe Financial Sector Index. European Financials are reaching a critical level around ~$20 (displayed on the chart below). The index has tested this level multiple times in the last 24 months. Many technical analysts are noting that if European banks break out above this level and resolve higher, it is difficult to be bearish on global equities. European banks are currently a very risk-on area of the market and tend to outperform during early-stage cyclical bull markets. The recent outperformance in Financials is not solely due to the tailwind from interest rates and it’s not just happening in Europe. Banks all around the world have been very strong in 2021. This is a global trend!

Do Interest Rates Need Time to Cool Off?

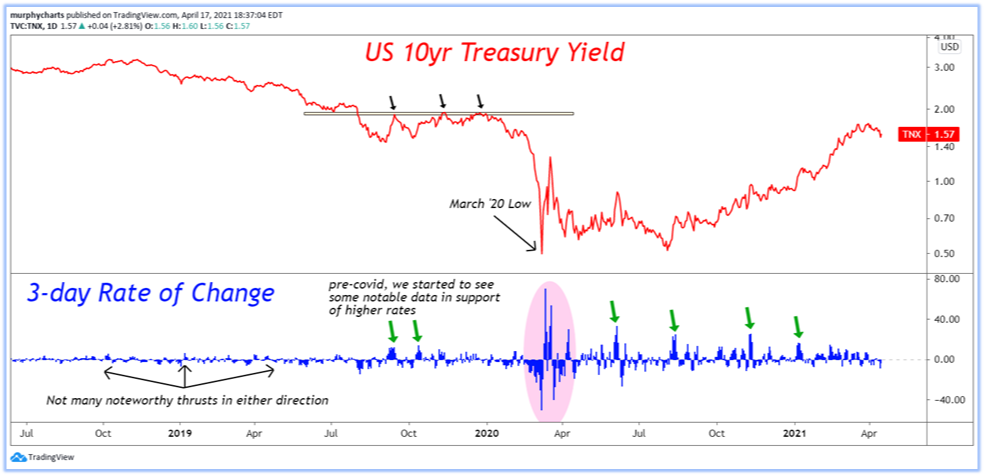

Thus far in 2021, benchmark yields have risen dramatically. However, to provide some perspective, they are only back to pre-pandemic levels. The recent move higher has aided sectors like US Financials and hurt areas like Technology, which are trading at much higher multiples.

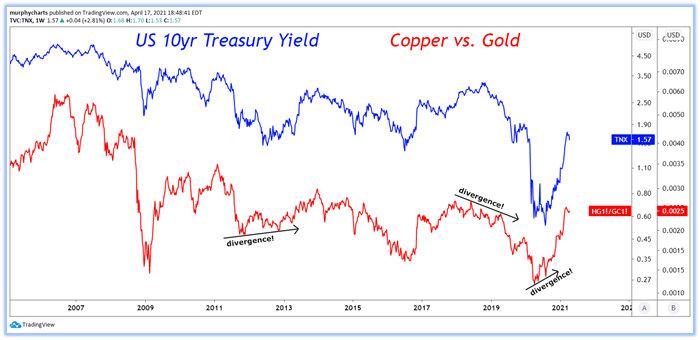

We love turning to the Copper vs. Gold ratio when it comes to analyzing interest rates. The Copper vs. Gold ratio simply takes the price of copper futures and divides it by the cost of gold futures. When the ratio is moving higher, copper is outperforming, when it is moving lower, gold is outperforming. In inflationary environments i.e. when inflationary forces trump deflationary forces and the economy is booming, commodities like copper are in high demand. Thus, the price of copper can increase substantially.

Gold has a very strong inverse correlation to real yields (interest rates that account for inflation). If real yields are moving higher, it will be viewed as a headwind to gold. The only datapoints we are looking for is if the copper/gold ratio is diverging from the direction of yields. If so, this would indicate that the path of least resistance is “to be determined”. Technical analysis is not a forecasting tool. There is no crystal ball. When reviewing price charts, we take a weight of the evidence approach which aids us in developing a thesis on the broad market. Thus far in 2021, the copper vs. gold ratio is yet to diverge from US 10yr yields.

Defensive Sectors Are Worth Our Attention

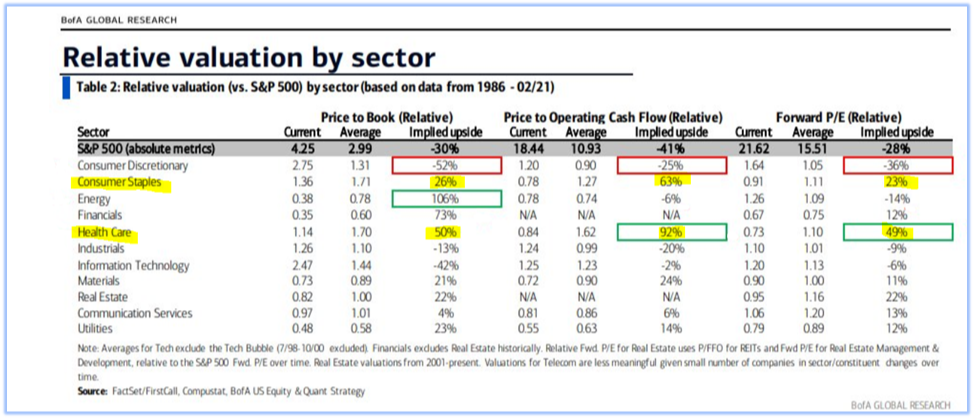

With benchmark stock indices breaking out to new all-time highs, the defensive and less “flashy” sectors, specifically healthcare and consumer staples are not receiving much love. However, we believe now more than ever they deserve our time and attention. Not because we believe these areas of the market will outperform in 2021 and not because they offer the most attractive growth prospects for long-term investors - but because we find ourselves in the ~10th year of a secular bull market and these sectors offer attractive relative valuations.

To couple the attractive implied upside of these sectors, their relative strength charts, which are ratios that use the sector index as the numerator and the broad market (S&P 500) as the denominator are piquing our interest. Just take a look for yourself! Coming into the GFC recovery, healthcare underperformed, but by mid-late cycle, it began to really pick up some steam relative to the broad market. Industries within healthcare, primarily pharmaceuticals and providers may be worth taking a closer look.

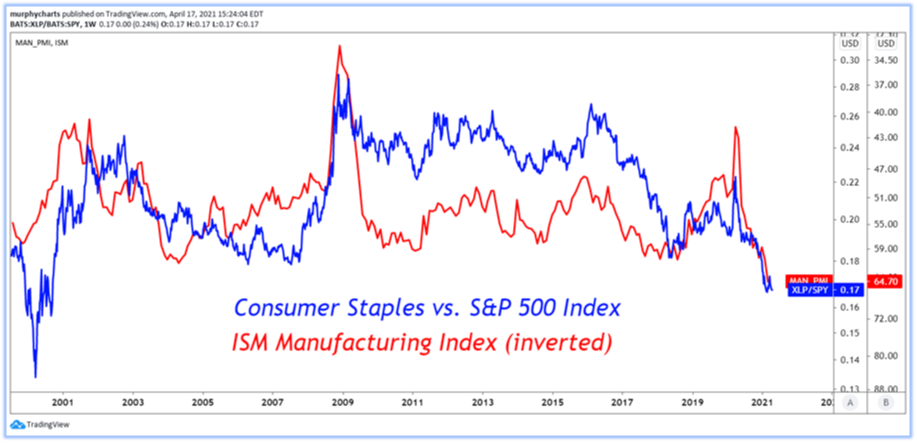

Another interesting chart is the Consumer Staples sector relative to the broad market, overlayed with the ISM Manufacturing PMI on an inverted scale. ISM PMI is a great gauge for the manufacturing strength/trend of the US economy. It is very correlated to the year over year performance of the S&P 500 index. With blowout numbers coming from ISM PMI, it makes one wonder if now is the opportune time to hedge your portfolio with some lower beta consumer staples names.

These two sectors aren’t as flashy as technology or discretionary, but they are quality US large-cap companies and many of them abide by our core investment philosophy which is grounded in dividend growth and strong balance sheets.

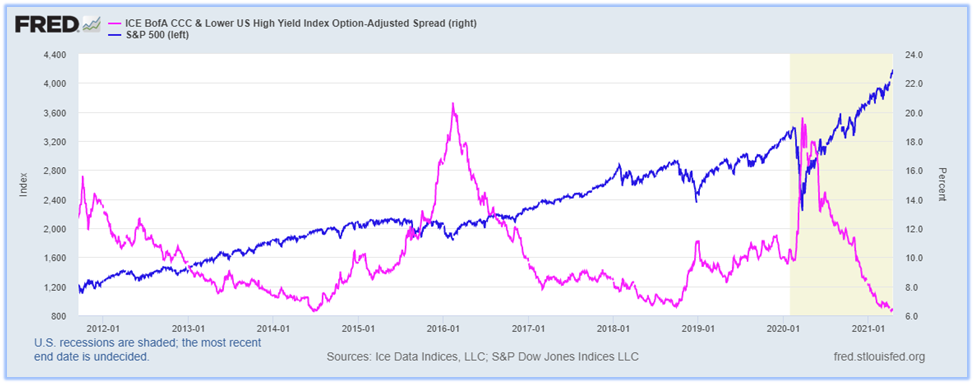

Closing Thoughts [Chart of the Quarter]

We hope you enjoyed the first edition of the MRA Technical Corner. Every edition will close with a “Chart of the Quarter”. This quarter we have the ICE BofA CCC & Lower US High Yield Index. The high-yield bond spread is the percentage difference in current yields of CCC graded & lower bonds compared against a benchmark treasury yield. When faced with poor to worsening economic conditions investors tend to flock to the safety of US Treasury bonds and away from Corporate bonds. This causes US treasury prices to rise and yields to fall and corporate bond prices to fall and yields to rise. In effect the spread between Corporate bond yields and Treasury yields widen or increase (Look at March 2020 for an example of widening spreads). The below chart displays a continued narrowing (going down) of the spread. Investors are requiring less reward (yield) for the added risk of lower quality debt. This indicates a healthy market as investors are not running to the safety of US Treasuries, but would prefer to hold onto riskier Corporate bonds with higher yields.

A lot of crazy things have happened in 2021 so far. Archegos Capital blow up, Gamestop mania, Crypto moving higher, equity flows spiking…Yet the credit market is giving the greenlight to the equity market (for now). If any of the above-mentioned events were to bleed over into the broad market and increase systematic risk, high yield spreads would not be narrowing to new lows.

This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.