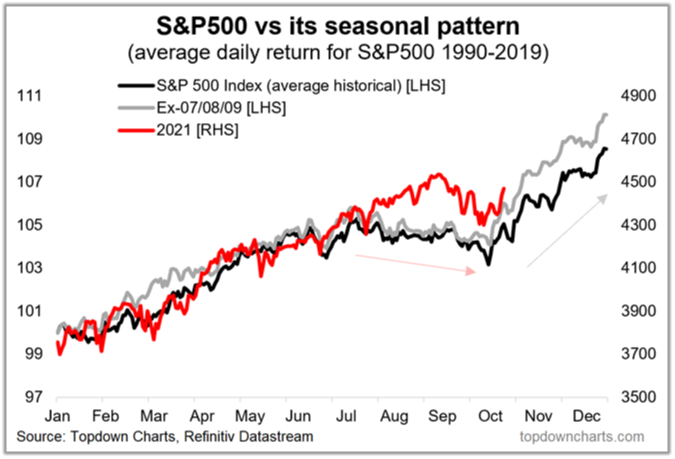

We find ourselves in the heart of earnings season as US stocks continue to print new all-time highs. The story of Q3 was not one of market euphoria or investor complacency. Rather, the true story consisted of seasonal trend, bond pessimism and China equities. Let us begin with seasonality. Below, is a chart of the average daily return for the S&P 500 from 1990-2019 (black line) overlayed with the index’s price path for 2021 (red line). The month of September is a seasonally weak period for stocks. Typically, we see this weakness fade in early to mid-October, followed by a strong finish to the year. It’s mind boggling how similar 2021’s price path is to the seasonal pattern. However, seasonality is just one piece of information. Although interesting, if seasonal trends held such a strong predictive power, forecasting returns would be simple and our jobs as wealth managers would cease to exist! As we’ve stressed in previous write ups, it’s just one datapoint.

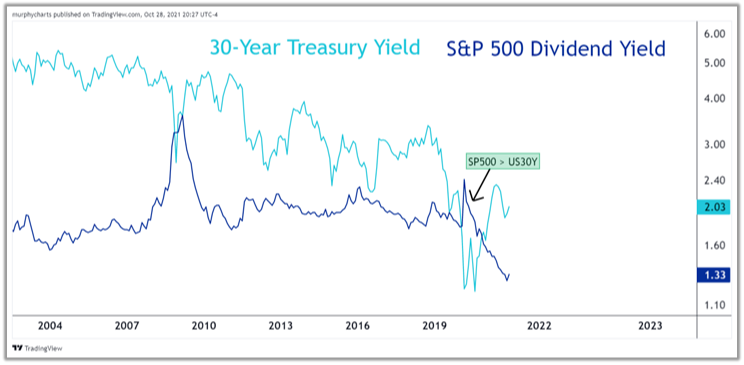

Next, we have the pessimism in bonds. It’s no secret that expected returns for bonds are the worst they’ve been in a very, very long time. With starting yields being as low as they are, an investor seeking to capture return from appreciating bond prices is unlikely to realize a legitimate gain. It is our view that bonds provide two basic functions within our portfolios. One being the reduction of volatility i.e. downside protection, and the second being a source of income. With yields being so low, we find ourselves mainly benefitting from a reduction in volatility. Remember, it wasn’t too long ago that the S&P 500 dividend yield was higher than that of a 30-year US Treasury bond yield. It’s crazy to think about, but this is the environment we are operating within. Yields are low and risk appetite for equities is high.

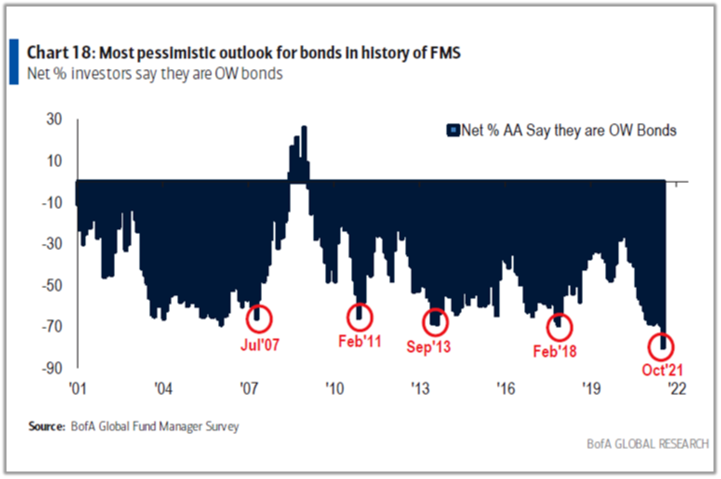

Over the past few years, we’ve witnessed investors take a step up on the risk ladder, assuming more risk in order to obtain desired yield. Whether its lesser graded debt, junk bonds, preferred stocks or even quality yielding equities - investors have been forced to go outside of the fixed income asset class in order to obtain adequate yield. It is without debate; bonds are the most hated asset class of 2021. Below is a chart depicting the results of the recent Bank of America Fund Manager Survey (FMS). The FMS asked managers if they were overweight bonds, and the results were staggering. The lowest net percentage reading in the survey’s 20+ year history. Now it is important to note, this doesn’t mean that bonds do not play a role in one’s portfolio. Quite the contrary. Just because a fund manager isn’t overweight bonds doesn’t mean he or she does not include them in their portfolio.

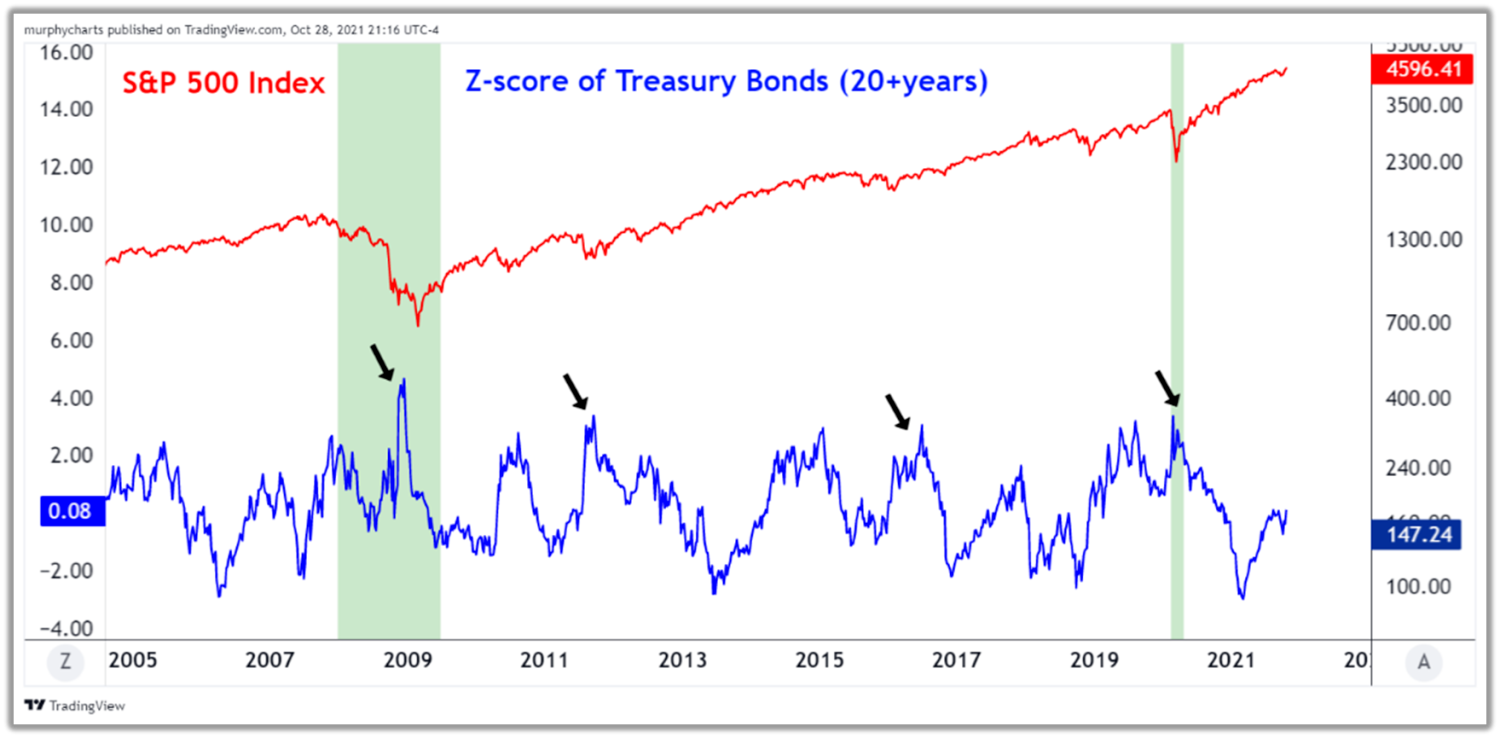

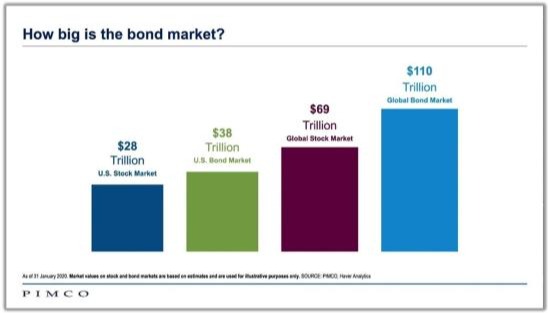

From a portfolio construction perspective, US bonds will always have a seat at the table. Whether it’s an exogenous shock like the COVID-19 pandemic or an endogenous decline like that of the great financial crisis, when investors fear economic deterioration, they flock to the safety of the world’s most reliable asset class. Below is a chart depicting the 1yr Z-score of long-dated treasury bonds overlayed with the S&P 500 Index. Notice that during recessionary periods (shaded regions) bond prices rise. In risk-off environments money will flow away from equities and into the safety of US bonds. It may not pay to be overweight bonds in a rising interest rate environment, but they are still necessary when it comes to building a quality retirement portfolio. There’s a reason the US bond market is 35% larger than the US equity market. Demand for US government bonds, never ceases to amaze us!

Lastly, we’d like to touch on the recent headlines coming out of China. The potential default of China real estate giant Evergrande sent waves of fear throughout the investor community. Pundits were quick to compare the fiasco to that of the Great Financial Crisis. A time where a collapse in the real estate sector nearly took down the global banking system. Many of our clients wondered if this was a just comparison. The answer is no. Commonwealth CIO Brad McMillan, CFA said it best in his recent blog post. “Is this news worth paying attention to? Certainly. It’s scary stuff, if true. Is it worth worrying about? No, not yet. The fact is that there are significant differences between both the situation then and the situation now, as well as between the U.S. position in global financial markets and the Chinese position. When you add those details up, the situation does not look nearly as scary.” The fact of the matter is, China’s equity market was already displaying an incredible amount of relative weakness due to geopolitical risks, prior to Evergrande’s potential default hitting the newswire.

All things considered, China is an economic powerhouse and although their growth has decelerated in recent years, it is still growing at a tremendous pace. The potential default of Evergrande, may or may not have larger implications on global risk assets – but for now, there is no evidence support such effects.

We hope you enjoyed this edition of the Technical Corner Newsletter. If you have any questions or would like to discuss the above in more detail, please reach out and let us know!